Forced, planned and unexpected transformation

09 November 2021

Newsletter by the Private Wealth Management Team

Reading time: 2 minutes

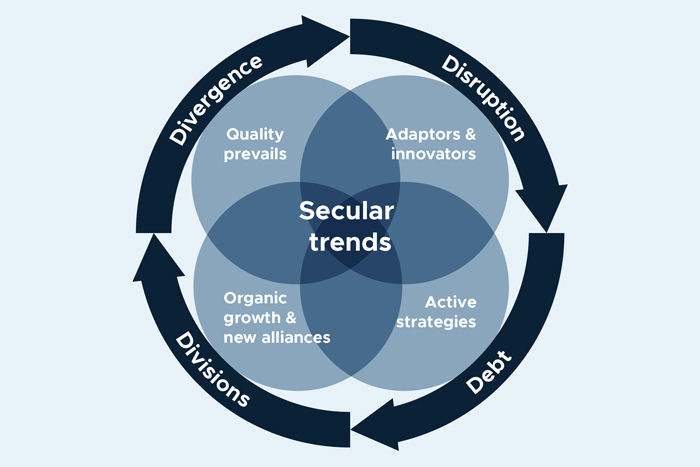

In the year 2022 and beyond, we believe that the global economy and global markets will undergo forced, planned, and unexpected transformations on a scale unlike anything witnessed in recent history. Only select economies will be able to quickly adapt, innovate and thrive, experiencing broad, overall growth.

The change and transformation in motion will remain in play for the foreseeable future. Formidable forces are driving this transformation, creating tremendous disruption, divergence, and divisions in an age of debt levels at historic proportions in nearly all emerging and advanced economies.

While pandemics and crises pose significant threats, they also trigger great innovation, adaptation and thus positively transform our world. However, not all governments and organizations are able to adapt, innovate, and change fast enough.

Widespread divergence and disruption across economies and industries is a by-product during periods of transformation. Organic growth will surface more readily in countries with the most business-friendly and adaptive environment, especially those primarily driven by domestic consumption. At the same time, new alliances will forge stronger trade relationships or fortify old trade routes. Quality countries and companies that can adapt and innovate will thrive.

Investment strategies and portfolios must be constructed or adjusted accordingly. Indeed, portfolio managers will need to adopt a more active portfolio management style for the year ahead.

Why we’re “risk-on”

We remain “risk-on” — searching for return, willing to take risks due to three critical supporting variables: Growth, policy support and negative real yields.

- Growth — Key advanced economies (US and EU) will continue to grow, albeit slower than the post-pandemic bounce, recovery. The US will have more organic, domestic-driven growth, thus our favourite region.

- Policy support — While there are growing risks of tapering monetary policy accommodation in the quarters ahead, it will take place from historic levels of policy support. Therefore, the policy will be moving from ultra-supportive to very supportive.

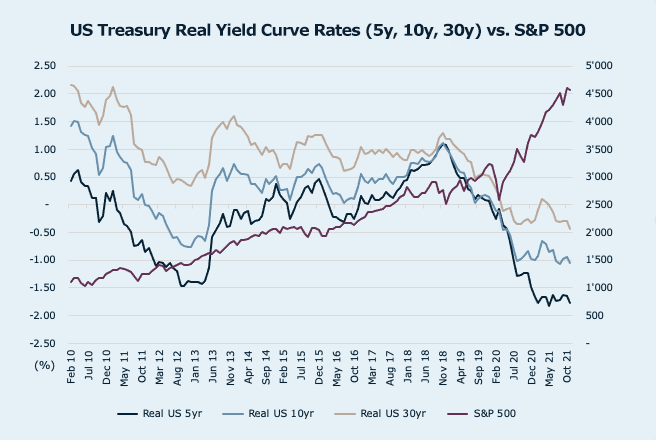

- Negative real yields — In a world where most of the core government bond real yields are negative, investors will likely continue to allocate to riskier assets with positive real yields; riskier parts of fixed income, and into equities, and other investments.

Portfolio positioning

Overweight equities, primarily US, EU, and Switzerland, favoring cyclical sectors, value, and quality style factors. In hedge funds, we prefer allocation to credit and equity long/short, event-driven, and global macro strategies. We continue to favor distribution to solid and active managers and allocation to structural trends. Lastly, we hold a strong overweight in our gold allocation given our concerns about the geopolitical and inflation outlook and remain positive on the USD outlook.

See our asset class views.

Important notice

The information provided herein constitutes marketing material, that may contain general information, and has been prepared by personnel in the GMG Investment Solutions SA or GMG Institutional Asset Management SA (collectively “GMG”) and is not based on a consideration of the prospect’s circumstances. This document reflects the sole opinion of GMG or any entity of the GMG Group and it may contains generic recommendation.

Non-Reliance: This document does not constitute a recommendation or consider the particular investment objectives, financial conditions, or needs of individual clients. Before acting on this material, you should consider whether it is suitable for your circumstances and, if necessary, seek professional advice. GMG is not soliciting any specific action based on this material it is solely intended for illustration purpose.

This document is not the result of a financial analysis and therefore is not subject to the “Directive on the Independence of Financial Research” of the Swiss Bankers Association.

This document is neither a prospectus as per article 652a or 1156 of the Swiss Code of Obligations, a listing prospectus according to the listing rules of the SIX Swiss Exchange or any other exchange or regulated trading facility in Switzerland, nor a simplified prospectus, key investor information document or prospectus as defined in the Swiss Federal Collective Investment Schemes Act. Any benchmarks/indices cited in this document are provided for information purposes only.

The accuracy, completeness or relevance of the information which has been drawn from external sources is not guaranteed although it is drawn from sources reasonably believed to be reliable. Subject to any applicable law, GMG shall not assume any liability in this respect.

Risk Disclosure: This document is of summary nature. The products referred to herein involve numerous risks (including, without limitations, credit risk, market risk, liquidity risk and currency risk). In respect of securities trading, please refer for more information on such risks to the risk disclosure brochure “Risks Involved in Trading Financial Instruments – November 2019”, which is available for free on the following website of the Swiss Bankers’ Association: www.swissbanking.org/en/home.

Material May Be Outdated: This material is produced as of a particular date. Accordingly, this material may have already been updated, modified, amended and/or supplemented by the time you receive or access it. GMG is under no obligation to notify you of such changes and you should discuss this material with your GMG relationship manager to ensure such material has not been updated, modified amended and/or supplemented. The market information displayed in this document is based on data at a given moment and may change from time to time. In addition, the views reflected herein may change without notice. No updates to this document are planned. In the event that the reader is unsure as to whether the facts in this document are up to date at the time of their proposed investment, then they should seek independent advice or contact their relationship manager at GMG.

Information Not for Further Dissemination: This document is confidential and should not be reproduced, published, or redistributed without the prior written consent of GMG.